- info@sentinelindia.in

- 9871158158, 9810004134

Does it makes any sense to buy “Return of Premium Term Plan”?

The one-line answer is “NO – it does not make sense”

A “Return of Premium Term Plan” or TROP as its called – pays back all your premiums at the end of the period, whereas the plain term plan doesn’t return back anything. Before we get into the analysis further, I want you to know why these return of premium term plan came into existence!

Term plans have become very popular in the last few years. We are seeing so many advertisements screaming about term plans importance. However, a lot of investors who don’t understand term plans fully, still feel a pinch that their premiums get “wasted” if nothing happens to them.

They equate “paying premiums” as “losing premiums” if they dont die. They compare it with an investment policy (read traditional insurance plans) where they get back there a sum assured towards the end of the policy.

Insurance companies sensed this behaviour and they introduced something called “Term Plan with Return of Premium” which can now proudly tell customers that they have nothing to lose. They get claim money on death, and if they don’t die, they get back all their premiums paid. Many investors who do not understand the time value of money concept fall for a product like this, as to human mind “getting back all your premiums” sounds very attractive offer.

Now, let’s talk about why it does not make sense as a product.

The premium for the TROP (return of premium term plan) is higher than the plain term plan and it can be 2x-3x times the normal premium in some policies.

So basically, you are paying an extra premium for getting your premiums back after 30-40 yrs!

Let’s look at an example of a 30 yr old male, who wants to buy a 1 crore term plan till 60 yrs of age (for 30 yrs tenure). In which case the premiums are as follows (Example is of Max Life Term Plan as on 21st Dec 2020)

| Type of Plan | Yearly Premium | Details |

|---|---|---|

| Simple Term plan | Rs 9912 | One has to pay Rs 9912/yr for 30 yrs for Rs 1 crore cover. You don’t get back anything at the end on survival |

| Return of Premium Term Plan | Rs. 17,969 | One will have to pay an extra amount of 8057 for 30 yrs (apart from 9912) and will get back Rs 5.01 lacs (this is all premiums paid excluding the tax amount) at 60th year |

If you look at the example above, you can see that in both the plans you are paying Rs 9912 for the Rs 1 crore cover. Only difference is that in second policy, you are paying an extra Rs 8057 to get back Rs 5.01 lacs (excludes the taxes part) at the end. This is the only difference between the two versions.

So internally, the term plan with return of premium is simply a bundled product of a normal term plan and an investment policy. If we ask what is the return of this investment policy where you are paying Rs 8057 per year and getting back Rs 5.01 lacs after 30 yrs.

The answer is 4.05% CAGR.

Yes, its barely above saving account rates and a little below a normal fixed deposit interest.

I did the same analysis for the tenure of 40 yrs and 50 yrs policy (read why you should not take such a long tenure term plan) and the IRR return was 3.92% and 3.00% respectively, which means that if you buy the policy for a longer tenure, the return gets lower and lower and the product becomes even worse.

Below is the IRR return calculated in an excel sheet for your reference

Note : The above calculations are done in Excel for just one company plan, however similar kind of numbers are expected from other companies return of premium term plan. Please do IRR calculations yourself if you looking at other companies plans.

What do you do, if you want to stop a “Return of Premium Term plan” in-between? Let’s say after 10 yrs?

It will not be as simple as a normal term plan, because, with the return of premium policy, your mind will tell you that you just have to continue it for another 20 yrs and you will get back all your premiums. Very smartly, the insurance company has converted a pure term plan into an “investment policy cum term plan” with very bad returns.

so the better alternative than a “term plan with return of premium” is to buy a simple term plan (here are 20 checklists before buying term plan) and invest the extra amount in another investment products like PPF, FD’s, Equity mutual fund or debt mutual fund and you will have better flexibility and returns.

Check out this video from Subramoney talking about this product

What happens if you stop paying a premium for Return of Premium Term plan?

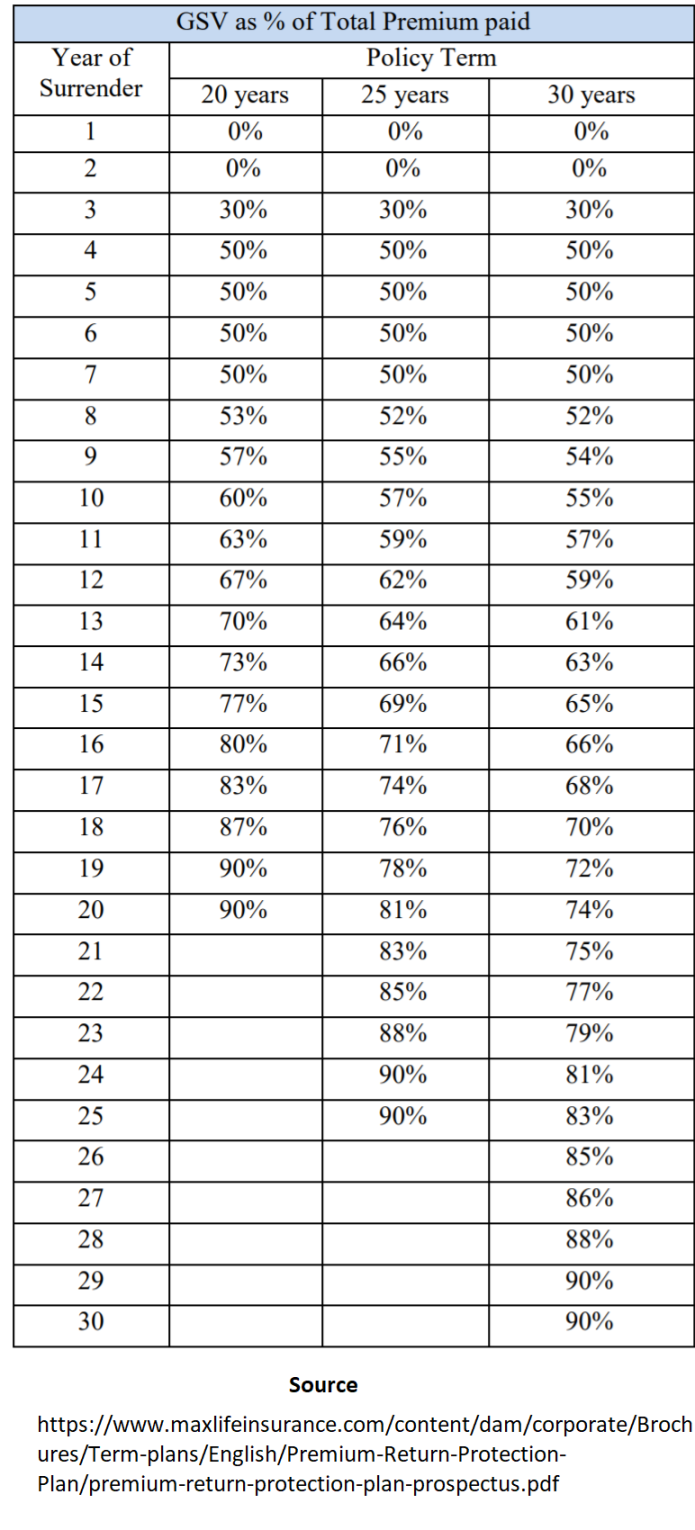

There is an option to get a surrender value if you stop paying the premiums in between. Just like traditional plans, there is the concept of “Guaranteed Surrender value” in these kinds of policies which comes into picture once you have paid 3 yrs premium. However, the amount you get back is a fraction of what you have paid. There is a percentage assigned for every year which tells what part of the premium paid will you get back if you surrender the policy in a year. Below is a snapshot of the chart taken from Max Life Brochure

So, as per this chart – if one wants to surrender the policy in 10th year, they will get back only 55% of the premiums paid (excluding premiums).

Some other Info

So TROP is a very carefully designed product which favours the insurance company but makes the product look very good and works on the psychology of the investor. Better stay away from it. The best idea is to buy the simple term plan with the lowest premium.

If you have already invested in this kind of plan, then you need to evaluate what will make sense for you!

Do let us know if you liked the article and does it make sense to you? Share in the comments section!